You know what’s cool? A trillion dollars.

That was the market capitalization of Facebook just over a year ago, right before the company decided to rename itself Meta. It has since declined by roughly $800 billion.

Eight hundred billion dollars! That’s more than the market cap of almost every company in the S&P 500. It’s more than

Exxon Mobil.

It’s more than

Berkshire Hathaway.

It’s more than

Tesla

and a parking lot of Tesla cars.

The recent tech selloff has shrunk Amazon, Alphabet and every giant but

Apple,

wiping out trillions of dollars across Silicon Valley with a brutal efficiency that only an engineer could appreciate. But no company looks as dismal these days as the one whose stock price is down 75% since last September. The good news for

Meta

META -4.89%

is that many of the biggest losers in recent market history learned how to win again. The bad news for Meta is that it doesn’t have much else in common with them.

Many companies change strategies because they lost money. Meta is losing money because it changed strategies.

It has been almost exactly one year since chief executive and co-founder

Mark Zuckerberg

made the bold maneuver of rebranding Facebook as Meta Platforms because he believed the future of the company was not in social media but the immersive, amorphous online realm known as the metaverse.

The decision to place so much faith in such an unproven premise will go down as one of the riskiest bets any corporation has ever made, no matter what happens next. But what’s happening now is bleak. It’s still not clear what might count as success, only that Meta is nowhere close to it—and the company has gone about getting there in the wrong way.

“You want to take big problems and break them down so that you have small wins and small losses,” said

Sim Sitkin,

the

Michael W. Krzyzewski

distinguished professor in leadership at Duke University.

Meta CEO Mark Zuckerberg wore a fencing outfit during an event announcing the company’s shift to the metaverse.

Photo:

Michael Nagle/Bloomberg News

I called Dr. Sitkin because he wrote a scholarly paper a few decades ago about this strategy of small losses and coined a term for it: “intelligent failure.”

The evaporation of $800 billion in market value was not particularly smart by his standard, which is useful for thinking about Meta and other tech companies because of the nature of their businesses. Innovation requires experimentation. Experiments fail. Failure can be instructive.

Major success is the product of minor failures, but only if the experiments meet specific criteria. They should address worthy questions with uncertain answers. They should be meticulously planned and useful regardless of the results. And they should be modest. That’s the most important thing about them. The rewards are incremental because the risks are not existential.

Amy Edmondson,

a Harvard Business School professor and author of the forthcoming book “Right Kind of Wrong: The Science of Failing Well,” says the optimal bet size is hard to define but easy to describe.

“As small as possible,” she said. “Just big enough to be informative.” Then she put it another way: “You don’t bet the company.”

Meta didn’t exactly follow that advice.

Last year, Mr. Zuckerberg declared that he wanted Facebook to be a metaverse company. Last week, after Meta reported another grim quarter for earnings, the CEO reiterated that he still felt that way. He understood that “people might disagree with this investment.” He just happened to think they were wrong. “I think people are going to look back on decades from now and talk about the importance of the work that was done here,” he said.

They have a lot more work to do. My colleagues at The Wall Street Journal recently reported that Meta’s flagship metaverse had fewer than 200,000 monthly active users. There are more people who come to see the New York Mets.

But it doesn’t really matter that Mr. Zuckerberg’s view is as lonely as the metaverse. His control of Meta’s voting shares gives him an unusual form of power. “That gives us even more responsibility to push for it and do things that other people might not be able to do,” he recently told the tech site Protocol, adding: “I want to live in a world where big companies use their resources to take big shots.” (A spokeswoman for Meta declined to comment but pointed to Mr. Zuckerberg’s previous remarks.)

Others in his shoes might feel pressure to cut their losses. But it’s a good thing legs are coming to the metaverse because Mr. Zuckerberg is digging in his heels.

I haven’t spent much time in the metaverse—which, as it turns out, makes me like most people at Meta—and I have no plans to vacation there anytime soon. Neither does Dr. Sitkin. The metaverse has more appeal to him as a concept than a place to visit because it represents a “stretch goal,” as he calls it, or a seemingly impossible task that requires some kind of external circumstance or creative breakthrough to achieve.

But what really interests Dr. Sitkin is that companies avoid risk when they’re doing well and inhale risk when they can least afford mistakes. This is the paradox of stretch goals.

“Those who should pursue them don’t,” he said, “and those who shouldn’t pursue them do.”

Meta is an exception to that rule. It should pursue stretch goals. It did. The problem was that it stretched too far and its goal was too vague.

“You definitely want to have a parachute if you’re going to jump off a high cliff,” said Dr. Sitkin. “And you want to know if that cliff has a staircase going down—so you can do it one step at a time.”

‘I think people are going to look back on decades from now and talk about the importance of the work that was done here,’ Mr. Zuckerberg said in defense of the company’s strategy shift.

Photo:

BENOIT TESSIER/REUTERS

It’s entirely possible that Mr. Zuckerberg is right about the metaverse and the company’s stock price will be a bargain in the long run. A website he built from a college dorm room becoming one of the world’s most valuable companies also sounded crazy, and positioning Facebook for mobile at precisely the right time showed that he’s been able to peek around corners of social media that few other people can see.

But his latest vision requires squinting. Mr. Zuckerberg himself warned that it would take patience, trust and more than a few quarters of lousy financial results to figure out whether the metaverse bet pays off.

“This is not an investment that is going to be profitable for us anytime in the near future,” he said one year ago.

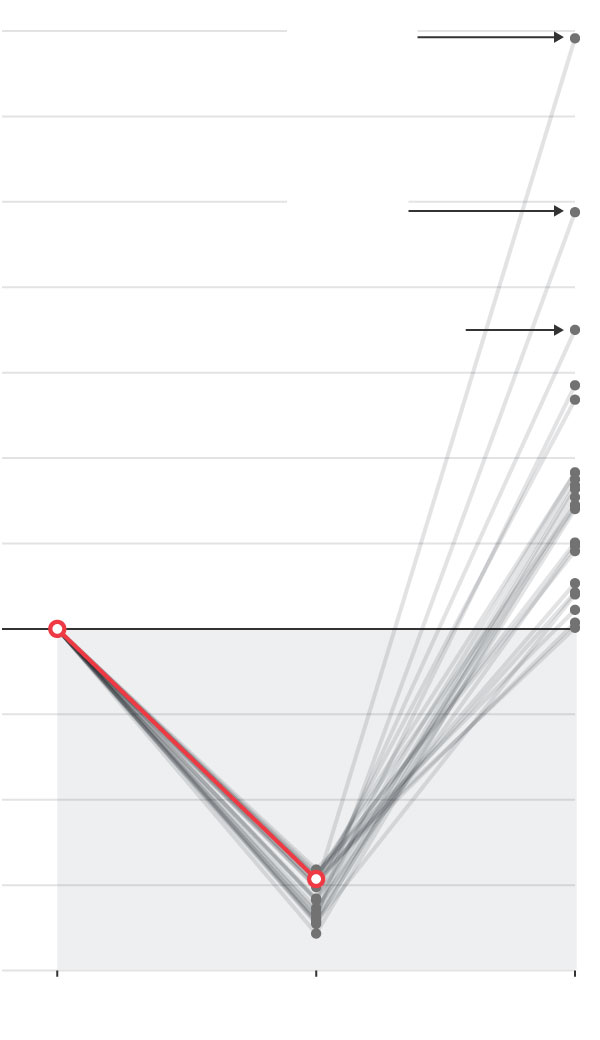

Since 2020, 23 S&P 500 companies have had their stock prices drop more than 70% in less than one year and then climb back to a new high.

Percentage change from previous high

That prediction turned out to be accurate. The operating losses of its metaverse division amounted to $3.7 billion last quarter alone, and Meta’s chief financial officer said that he anticipates “operating losses in 2023 will grow significantly.” The market reacted appropriately to this comment: It freaked. Meta is now trading at its lowest price since 2016, when TikTok was a sound that clocks made, and the company has shed$23,000 a second in market cap from last year’s peak.

The financial incentives for intelligent failure get stronger the faster a company grows. The price of the all-or-nothing bet on nascent technology that Mr. Zuckerberg made from his dorm room was low in dollar terms. Now it’s humongous.

But a surprising thing about companies that have been in Meta’s position is how many of them made their money back. In fact, nearly two dozen S&P 500 companies have recovered from being down 70% in one year since 2020 alone, according to Dow Jones Market Data research.

Most of those losses were the result of broader forces beyond the control of those companies. The pandemic crushed department stores, but Macy’s and The Gap are back above their prepandemic stock prices. Energy stocks were pounded when U.S. oil futures briefly ducked below zero, but Halliburton and Occidental Petroleumrecovered from the lows and climbed back to previous highs.

Meta has plenty of headwinds in the real world, too. The economy is gloomy and interest rates are rising. A bitter dispute with Apple bruised Facebook’s advertising business as competition with TikTok cut into Instagram’s popularity. But what makes Meta different from the survivors of stock tumbles is what caused them to begin with. Theirs were external shocks. This one was self-inflicted.

It’s appropriately meta that the most compelling explanation for an $800 billion free fall is in the name of the company. That may be a failure not intelligent enough to be a success.

Write to Ben Cohen at ben.cohen@wsj.com

Copyright ©2022 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

{kind=link}